Fed tightening view supports USD It

looks like people are starting to come around to my view of what the FOMC

minutes imply. Equities were down around the world while credit also suffered.

Fed Funds expectations and bond yields initially rose, then fell back to trade

lower as equities came off. In the US, the employment cost index rose 0.7% qoq

in Q2, up sharply from 0.3% in Q1 and exceeding estimates of 0.5%. This is the

highest rate of increase since the financial crisis of 2008 and made people

think that perhaps there isn’t as much slack in the labor market as had been

thought. Less slack in the labor market would mean earlier tightening by the

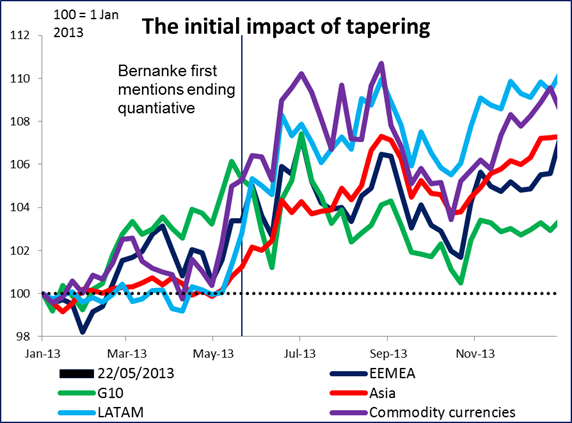

Fed. It seems we are starting to repeat on a small scale what happened back in

May 2013, when then-Fed Chairman Bernanke started to talk about ending the

Fed’s quantitative easing program. Back then the dollar rose broadly against a

wide variety of currencies. I would expect to see that performance repeated,

although perhaps not quite on the same scale.

The dollar continued to gain all around even though US interest

rates and rate expectations barely moved on the day. There was one big

difference between yesterday and recent days, though, and that was the collapse

of EM currencies. USD/EM had gained somewhat on Wednesday, but on Thursday the

dollar just soared against almost every EM currency we track. It was up 1.7% vs

IDR, 0.8% vs HUF, INR and BRL, 0.7% vs THB, etc. Oddly enough RUB held up

relatively well; USD/RUB was up only 0.2%. We are seeing EM weakness rather

than just USD strengthen as EUR/EM moved almost as much as USD/EM. The move

have been in reaction to tightening expectations, as mentioned above, or it may

have been due to the Argentinian default, which adds to the Russian sanctions

to remind investors of the potential risks in the EM world. (Although let’s not

forget that several Eurozone countries were near default recently, too. People

with carry trades on should be careful as these sorts of carry trade unwinds

can go on for some time. Over the longer term I would expect EM to bounce back,

as the yield gap is quite attractive with Eurozone yields at record lows, but

caution is warranted for now.

China’s official manufacturing PMI for July increased more than

expected, rising to 51.7 from 51.0 (market expectation: 51.4). The final

manufacturing PMI for July from HSBC/Markit on the other hand was revised down

slightly to 51.7 from 52.0. AUD/USD initially spiked when the former number

came out, then plunged ahead of the latter. It’s now trading lower, which

implies that the market believes HSBC/Markit more.

Today: It’s a PMI day in Europe as well. The day starts with the

manufacturing PMI figures for July from several European countries, the

Eurozone as a whole, the UK and later on, the US. As usual, the final forecasts

for the French, the German and Eurozone’s figures are the same as the initial

estimates. The UK manufacturing PMI is estimated to be slightly down to 57.2

from 57.5, while in the US, the ISM manufacturing PMI is expected to have risen

to 56.0 from 55.3, which could prove USD-supportive.

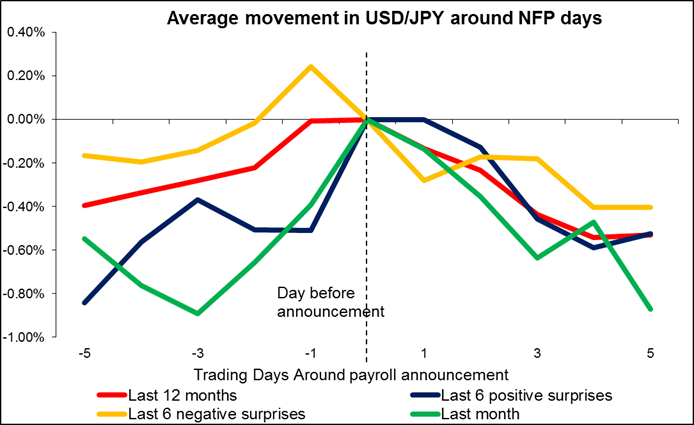

The main event though will be the US nonfarm payrolls for July.

The market consensus is for payrolls to rise by 231k vs 288k in June. A strong

NFP reading, along with an anticipated unchanged near six-year low unemployment

rate of 6.1%, should add to the recent solid US data and boost USD further. As

usual, I recommend that anyone wanting to take a position ahead of the figures

should express their view in USD/JPY, which tends to react more on NFP days

than EUR/USD. Although I must note that on average, over the last year USD/JPY

has been lower a week after the NFP than it was immediately before the figure

regardless of whether the figure beat or missed expectations! In fact USD/JPY

was lower a week later the last six times. The pattern seems to have been that

USD strengthens going into the figure on expectations that it will change the

market’s view entirely, but then when it doesn’t, prices revert to where they

were earlier. I hesitate to say that “this time is different,” but I think this

time at least the NFP figure only has to corroborate market thinking, not

change market thinking, in order to keep USD rallying.

No comments:

Post a Comment